Nov 25,

2015

Today, let’s talk about competitiveness pressures on industry under carbon pricing and how carbon pricing policy can be designed to address these concerns. And in particular, let’s take a look at how Ontario’s draft proposal for its cap-and-trade system considers these challenges. I’ll get (a little bit) into the weeds, but the implications are quite important for good policy, so bear with me.

Let’s start with the findings—in brief—of the report that Ecofiscal released last week:

The triple-T idea is to provide support for vulnerable industries through (for example) free permits or rebates tied to production. That means that emitters still have incentives to reduce emissions. But they don’t have incentive to reduce emissions by reducing their levels of production. The result is that production (and emissions) in Canadian provinces won’t simply shift to other jurisdictions, undermining the economic and environmental performance of the policy (aka leakage).

Still, there are reasons why policy-makers would want to limit this support only to those that really need it. For one, it means that government would generate less carbon revenue, which it might otherwise have used for other economically or environmentally beneficial measures (for example, reducing income taxes or investing in clean tech or productivity-improving infrastructure).

And further, subsidizing production in this way introduces new distortions into the economy, and can increase the costs of policy. It’s not helpful—economically or environmentally—to support sectors that can simply pass on their carbon costs to consumers. It just boosts the bottom-line of those industries.

Last week, Ontario also released draft design details for its coming cap-and-trade system, including approaches to permit allocation designed to address competitiveness problems. To what extent, then, is Ontario’s approach “targeted, temporary, and transparent?”

According to the draft document, 100% of permits for big industrial emitters (except for electricity generators) will be provided for free, at least for the first three years of the program.

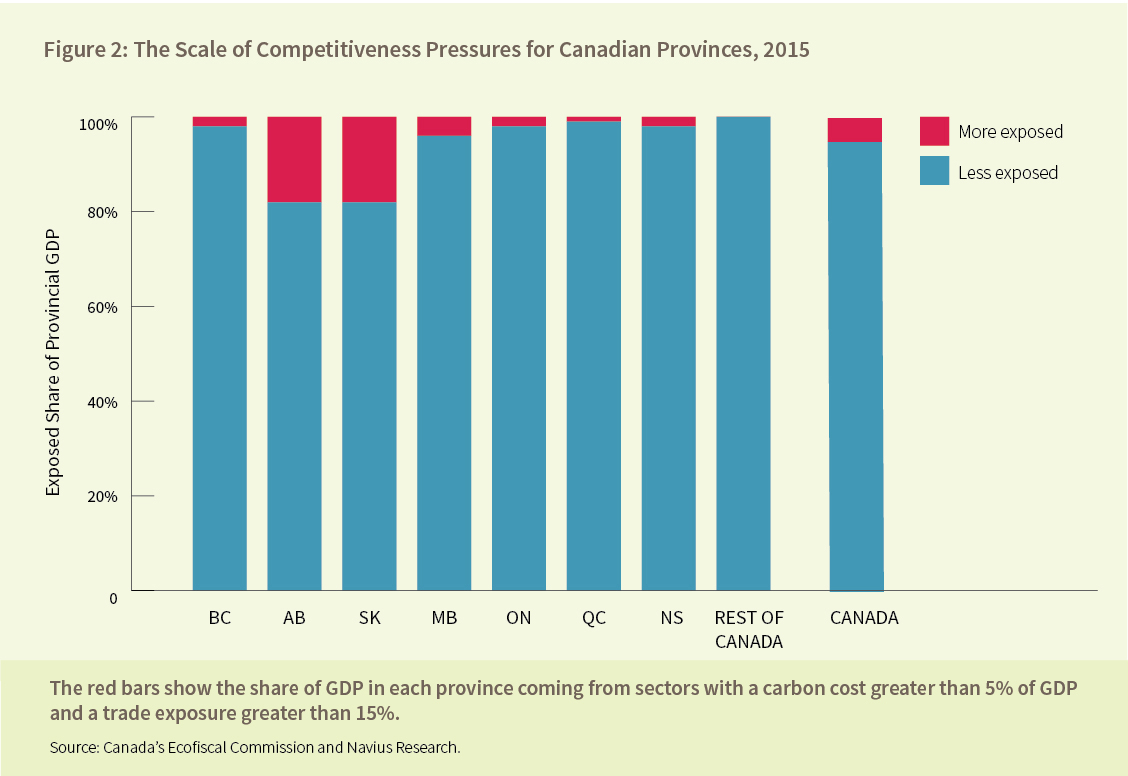

If the point is to address competitiveness concerns, is this level of support required? Our analysis suggest that only around 2% of Ontario’s economy is vulnerable to competitiveness pressures—and that’s at $30 per tonne CO2e, not the (approximately) $15 at which Ontario will start.

As the figure illustrates, only a few industries in Ontario have both high carbon costs and can’t pass on these costs to consumers. Without meeting both these criteria, industry won’t face competitiveness pressures.

Most manufacturing, for example, including vehicles and aerospace, compete in international markets, but aren’t particularly emissions intensive. As a result, those industries have low carbon costs. Commercial transportation can be emissions-intensive, but firms compete in local markets (all trucks must buy fuel within the province) so that means a level playing field. Most service sectors meet neither criterion: their carbon costs are low, and so is their trade exposure.

The longer term plan for free permit allocation after the initial 3-year period isn’t clear. There’s an important opportunity for government to respond to this issue following the current feedback period (which ends December 16th).

Here are the three big questions critical to address:

The discussion document suggests that Ontario will seek to target support measures, at some point, by adopting California’s approach of assessing leakage risk as medium, low, or high.

Like other approaches to assessing vulnerability, California considers both emissions intensity and trade exposure. However, it may not be the best tool for determining genuine competitiveness concerns.

California’s approach is much more generous in terms of free permits. It puts greater emphasis on emissions intensity than it does on trade exposure, but also has much lower threshold for emissions-intensity. If a sector has an emissions intensity of at least 100 tonnes of CO2e per million dollars of value added, it is considered at least medium risk for leakage—irrespective of trade exposure—and therefore eligible for free permits. That’s about equivalent to carbon costs of 0.3% of GDP, or well below the 5% used in our Ecofiscal analysis. The upshot is that the California approach broadens support to a much larger share of the economy.

The implication is that transitional support is being provided not just to provide support to vulnerable support, but to reduce costs for all big industrial emitters.

This kind of support arguably isn’t an efficient allocation of the value embedded in the emissions permitted created by the cap-and-trade system. It will reduce the cost-effectiveness of the policy.

Maybe such an approach can be justified as a way to ease the transition toward carbon pricing by reducing opposition from all, or most, industrial emitters? (The case isn’t clear-cut, because the stringency of the policy already provides a transition period: it starts at a low price that increases gradually over time).

But even so, if transitional support is the intention, Ontario would need to articulate a clear timeline for phasing out these supports. The options document suggests that allocation decisions for post-2020 will be made sometime after 2017. As a result, emitters can’t begin to make plans for a shift toward fewer free permits, because the details aren’t yet in play. That opens the door to demands for an even longer transition period of free permits. In short, it undermines the extent to which support will be temporary. But it also makes it less transparent, because it is unclear—both for the public and industries—who will continue to receive free permits and for how long.

Ontario got many things right in its proposed cap-and-trade policy design, including a number of the fundamentals. It adopts proven carbon pricing architecture from Québec and California. It covers a very broad range of Ontario emissions. The cap will decline predictably over time, and a price collar prevents excessive fluctuations in the carbon price.

But the details of allocation really do matter. These permits have substantial value. We should not give that value away for free without a very thoughtful and careful plan.

{kind=link}

1 comment

Manufacturing and mining of raw resources may be a small part of GDP and a high user of carbon; However, those industries produce the resources that the rest of the economy uses to operate. That being said their real contribution to economy is huge because it trickles down to the rest of the population to produce more economic activity. Cap and Trade will have profound negative consequences on the real wealth and well being of Canadians.

Cap and trade is a system that artificially creates a shortage of a resource. There are two choices for producers in the economy when faced with a shortage of a resource. They can become more efficient in using the resource while maintaining production levels, or they reduce production levels to use less of the resource. Efficiency can only be increased so much. There will come a point where production will have to be cut. Producing less value added goods means that the country as a whole will be poorer.

There’s a third and fourth option as well. One is to get out of the business of producing said goods, and the other is to stop using carbon. You can not produce steel, plastic, wood without a net gain in carbon emissions. Almost everything tangible is made up of these things, therefore the only conclusion is that the economy as a whole must shrink. Businesses will fail and there will be less products to buy.

Comments are closed.